Action Benefits

Action Benefits

2 min read

400,000 may lose Medicaid; Plan your outreach with these resources

An agent’s guide to Michigan’s Medicaid unwinding resources Good news for Michiganders: According to Georgetown University[i], we’re one of 10...

-1.svg)

2 min read

An agent’s guide to Michigan’s Medicaid unwinding resources Good news for Michiganders: According to Georgetown University[i], we’re one of 10...

4 min read

You’re in your office, working away, when you get a call from an agent across the way. He mentions he pretended to have a dropped call with a client...

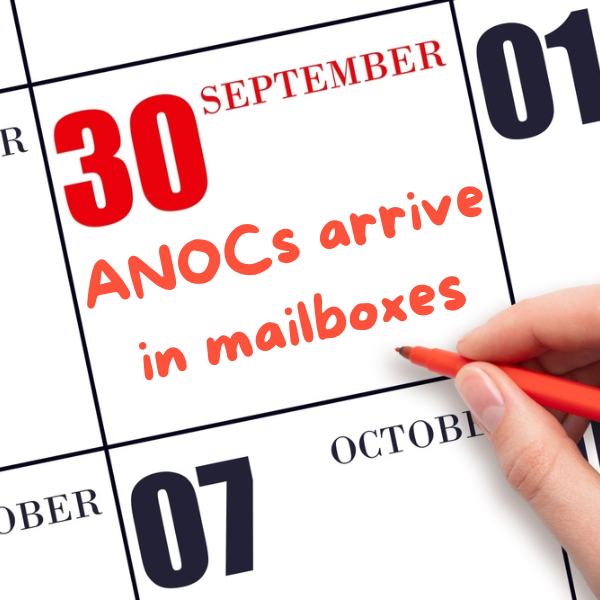

3 min read

Each September, Medicare carriers must send an Annual Notice of Change (ANOC) to their enrollees. The document is crucial – it explains changes to...