Action Benefits

Action Benefits

2 min read

Medicare Part D changes (again) in 2026: What health insurance agents should know

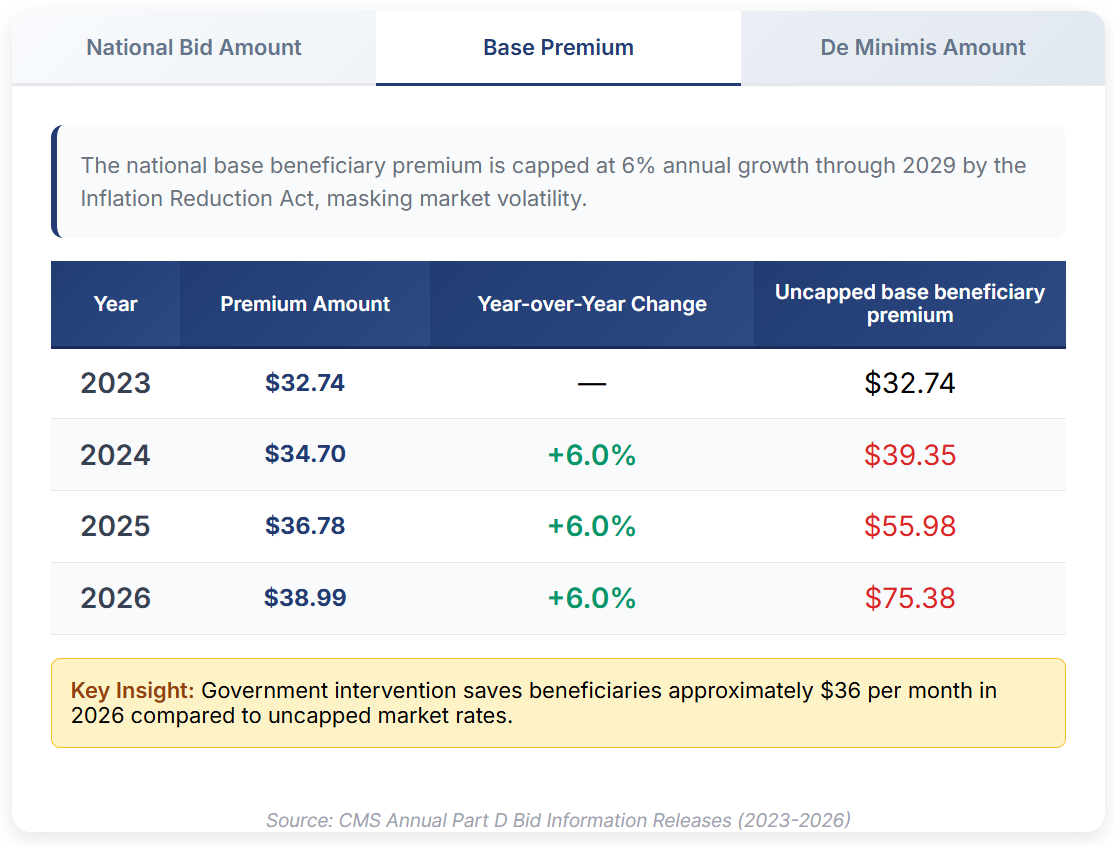

The 2022 Inflation Reduction Act kickstarted a long series of changes to Medicare Part D. Implementation of that redesign continues in contract year...

2 min read

The 2022 Inflation Reduction Act kickstarted a long series of changes to Medicare Part D. Implementation of that redesign continues in contract year...

%20(3)-2.svg)

2 min read

The plans, they are a changin’ The Medicare Advantage market has been shaken up all across the country, but particularly so in Michigan, and even...

2 min read

The Center for Medicare and Medicaid Services (CMS) has announced a new program designed to even the keel of beneficiary spending on prescription...